As the economic effects of COVID-19 continue to impact businesses across the country, banks have assured customers that they will continue receiving assistance through customer service portals.

“Call us and we’ll make it right,” Bank of America Chief Executive Officer Brian Moynihan said on CBS News’ “Face the Nation.”

But what happens during a financial crisis when banks are flooded with thousands of customers needing assistance all at once?

It’s not just big banks that are being overwhelmed.

Smaller banks and credit unions that lack technological resources and infrastructure are also struggling to keep up with the needs of their customers.

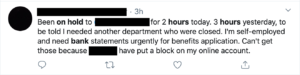

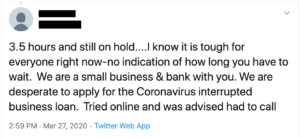

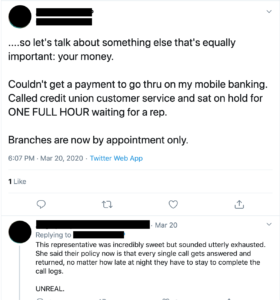

A quick search on Twitter shows more of the same: people in desperate need of assistance from their banks are being left on hold for hours on end.

The outdated technology and manual processes smaller banks and credit unions rely on to navigate the bureaucratic inner-workings of banking have left them under-equipped and underprepared for an economic disaster.

As the recession gets worse, more cracks in the banking system will emerge.

Bottlenecks, Pain Points, And Outdated Processes: How Can Automation Help?

Digital Process Automation or DPA is the means of digitizing and automating all of your processes. This is not just transferring all of your paperwork into the digital realm; you also need to streamline how you handle that data.

The overall goal is to reduce manual work. This reduction saves time and effort that would otherwise go into repetitive tasks. That means that loan officers and bank managers can focus on the upcoming crisis.

Problem 1: Manual Loan Application Request

If a customer wants to fill out a loan, they either need to do it on paper, over the phone, or by email. Any of these methods are time-consuming because banks need to vet potential lenders to ensure their credit is sufficient. In addition, these processes leave ample room for human error. Because there is a live person answering the phone or organizing the papers, there is a great danger of a high-risk borrower slipping through the cracks or for important information to get lost.

Having a handful of these applications is time-consuming; are banks and lending institutions ready to handle the sudden influx? At the moment, they are not. The number can potentially range in the thousands. Abrigo also notes that the federal government wants lending institutions to prepare borrowers for the upcoming crisis5, since financial hits may happen rapidly.

Solution: Smart Forms

Online lenders usually have the process partially automated. For this, they only need a single form that can handle a large volume of information. It’s not rocket science. Other banks, credit unions, and lending firms can implement the same forms. This saves time and effort because they don’t have to deal with piles of paperwork or email.

Virtus Flow can offer a one-page application online. This benefits the lender, the borrowers, and the internal users. We cannot automate the checking process because vetting customers for their credit is a necessity to prevent loan defaults, but we automate around it.

Smart Forms can dynamically move customers through complex processes like loan applications.

Problem 2: Slow Internal Processes

Even with the digital process going on, banks lack infrastructure by which to analyze thousands and thousands of requests per day. They also lack the means to refine their processes to save time and increase productivity.

Thanks to the restrictions of bureaucracy, manual and digital processes often become time-consuming together. Consider how long it takes for one person to check their work email; in a bank, that number grows exponentially. They also have to input data into spreadsheets, take notes during meetings, and type reports. How does one avoid such a grind?

Solution: Digital Workflows

Digital workflow is organizing processes into predictable patterns with data and different variables. This allows internal users to organize the tasks they need to complete during the day, and how to implement the data accordingly. The users can even choose which specific processes to automate for a particular day.

Virtus Flow specializes in digital workflows and the automation that accompanies them. One of our goals is to reduce the amount of digital paperwork, including emails and spreadsheets. This reduces the clutter that needs to be processed, organizing the data for easier analysis. We have designed them especially for banks to use.

Digital Workflows reduce the amount of manual labor required for simple tasks.

Problem 3: User Experience Feels Stuck In The Past

Despite what a customer may say, they may prefer fully automated systems. Many banks require customers to either wait for hours on the phone or for days in response to their emails. Phone bots can also prove frustrating when a customer wants an answer to a simple question.

Internal users also feel the same way. Thanks to changes in banking laws and financial regulations, more documentation is required. While we need this documentation for accountability, the current systems that handle this are not efficient for handling this. Workflows and information are not centralized.

Solution: Fully or Partially Automated System

Instead of using a machine to cut costs on using employees, implement the software so that customers can get their answers quickly. If you don’t need a human operator to handle customer complaints, then do a fully automated system. This will work when you need to work with multiple customers on loan risks.

Some banks may also prefer a partially automated system, where a human can step in and alter the process. This allows the user to change gears in the case of ongoing financial trends. As we don’t know for certain how long the outbreak will last, we need to prepare.

Fully or Partially Automated Systems can handle customer requests without human intervention.

Problem 4: Legacy Applications

Legacy applications cover core processes within the banking system. They also lack a simple means of integration or connecting with simple user interfaces or UIs. Many core processes are controlled by legacy applications that are hard to integrate with the rest of the new digital processes. This wastes time during the day that could be dedicated to output. Developing new connectors then becomes too expensive, which adds to a business’s tech budget. You lose time and money.

Solution: Integration through Robotic Process Automation (RPA)

RPA is the means of using intelligent technology and software to carry out repetitive tasks. Intelligent automation can handle clients’ credit cards, compile data, and organize it in a readable fashion. Knowbots are one such example, that gathers information online and presents them to the user.

Other processes like migrating data between systems can be automated as well. That would drastically reduce bottlenecks, by using robots. These bots follow a standard procedure to handle data. As an added benefit, they can also be programmed to consistently comply with government regulations.

Barriers To Automation For Banks And Credit Unions

Automation, when done correctly, saves time and improves efficiency. Everyone who is well-versed in tech knows that. But why haven’t banks already switched already, in preparation of potential influxes? There are actually more reasons than you think.

Overworked Personnel

Financial institutions hire dedicated employees to help improve customer satisfaction. These are not just the reps that answer the phones but also internal users that handle the banking or lending systems. They handle paperwork, IT tickets, and account issues. The people hired to handle these problems are highly qualified and trained to do their tasks. Unfortunately, they are only human.

Banks will suffer a lot in this recession because customers call to ask many questions about their accounts or car loans. Customer service will be overwhelmed and be unable to ask these questions. Employees will try their best, but the wait times will increase. As we have seen, this will lead to further complaints on social media and damages to banks’ financial reputations.

In addition, banks have not necessarily hired automation specialists. There are few employees that can balance integrating new processes into older institutions while conducting their daily tasks. Thus, they would need to outsource the services and would wait for fear of the increase in operational costs. Outsourced automation is only a trend in the 2010s, with a handful of firms like Virtus Flow handling key areas.

Complex IT Architecture

IT specialists use different systems for different things, many of which are old relative to developments in technology. When there are many moving parts, it can be difficult to integrate them smoothly. A high learning curve for certain software may not help for employees to receive the necessary training. Training eats into company time and may not account for different employees’ tech abilities.

The right Digital Process Automation software or partner helps all these systems communicate with each other and automates tasks between them. It also eliminates the need for training, thanks to the dynamic forms implemented. Only one user has to maintain it while other employees work with it.

DPA software should not require coding or other highly specialized skills. Any bank employee must understand how to use it and implement processes accordingly. That way any internal user can work with it. Dynamic forms are key to this efficiency and convenience.

No Cause to Overhaul Processes

Normally, banks lack the reason to make giant adjustments to their processes. By the time they do, the financial impact may have already made its mark. Changing systems means investing more money in technology and training.

During the previous recession in the late 2000s, many institutions closed or were merged. There was no time to save smaller banks or lending institutions. In this era, however, bank professionals and lenders have learned from the past. We cannot predict what will happen with the coronavirus outbreak, we can prepare for the worst while hoping for the best.

If they need to make changes, then they need to implement them fast. Automation tools now have a lower learning curve, and now is the time to get started!

The Answer: Using Virtus Flow Digital Process Automation Solutions

With our Virtual Workflows and Smart Forms, we can help banks, credit unions and lending firms survive these trying times. Your customer service employees and internal users will help more customers by cutting the time down on repetitive tasks.

Reach out to us today. With our DPA systems, you can increase productivity and reduce costs in the middle of this recession. Stay in business, and maintain the necessary cash flow as the virus spreads across the globe.

Resources

- University of Michigan Consumer Sentiment Index

- Econsultancy – Stats roundup: coronavirus impact on marketing, ecommerce & advertising

- What the new stimulus bill means for small business during coronavirus

- SBA – Coronavirus (COVID-19)

- Portfolio Management in Crisis: Coronavirus Implications for Lenders

We provide the help you need

One single solution to digitize your banking processes

Fast deployment and ROI, no disruption and no coding.